Recent data provide encouraging news about a key economic variable: labor supply, specifically, the share of Americans participating in the job market. Labor demand—as proxied by job creation, nominal wage growth, and job vacancies—has been unusually strong in the post-pandemic recovery. But analysts have repeatedly raised concerns about the supply of labor, specifically regarding the extent to which labor force participation would recover.

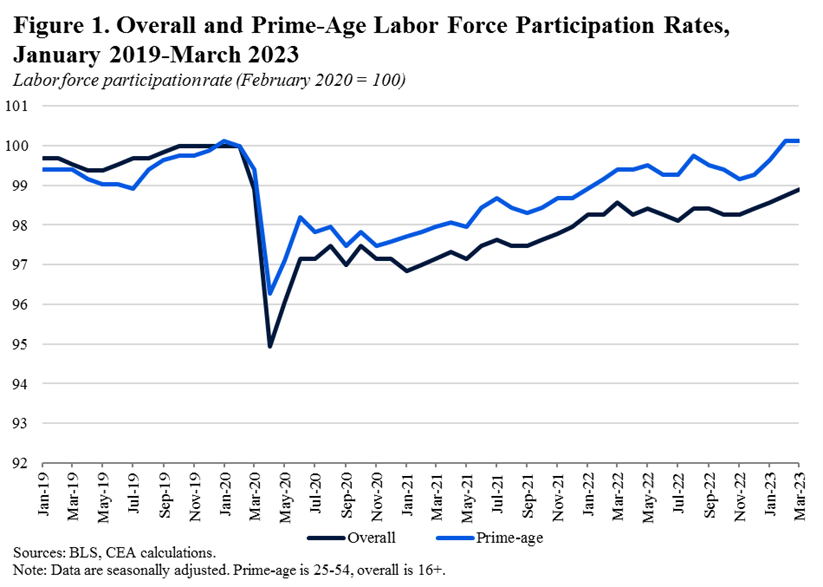

Recent trends, however, reveal that most of the “missing workers” are back in the labor market. Overall labor force participation is back to its pre-pandemic forecasted level, and the closely-watched prime-age (25-54) labor force participation rate is now a tick above pre-pandemic levels (see Figure 1). Immigration flows, depressed during the pandemic, have also rebounded. Job openings are also moderating somewhat, signaling that labor demand and supply are becoming better aligned, a necessary condition for achieving a path to stable and steady growth.

Throughout the economic recovery from the pandemic, there was much speculation about the “missing workers” who had not yet returned to the labor market. Numerous theories were offered to explain this apparent shortfall of workers. Analysts speculated that an epidemic of long Covid was keeping workers on the sidelines, that individuals were sitting out the labor market due to excess savings built up during the pandemic, that a “Great Resignation” was occurring as workers reassessed work/life balance or that the country had experienced a collective loss of work ethic.

Yet despite the enormous disruptions of the pandemic, these “missing workers” are now largely back in the labor market. The prime-age labor force participation rate, which had taken more than a decade to recover to pre-Great Recession levels, has now returned to those very high levels (see Figure 1). That labor force participation took only three years to recover to these highs is actually quite remarkable—and should reframe our thinking about the labor market in the aftermath of the pandemic.

The swift but lagged response of labor supply to surging demand suggests that with time workers do respond to favorable economic conditions. There are many plausible reasons that explain why this response is lagged. Most obviously, the job search process itself is not frictionless; it may take workers some time to find a good job. Also, if households adapted to the pandemic in ways that can take a while to unwind (such as giving up formal child care), this would delay the labor supply response to growing demand. That labor supply responds to improving conditions with a lag is also suggested by Cajner, Coglianese, and Montes (2021). They found that participation declines after a negative shock last about four years, with nonparticipants who return to school or shift to care responsibilities during the downturn accounting for much of the lagged response.

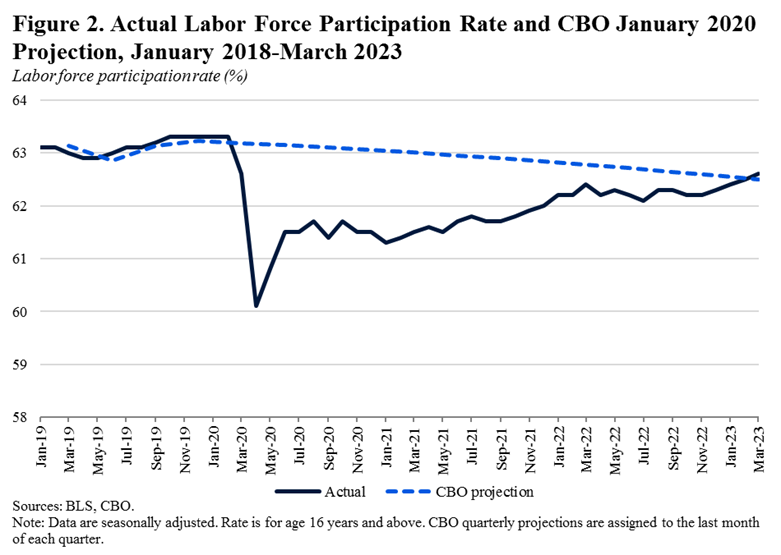

While prime-age participation is now above prepandemic levels, overall labor force participation has declined 0.7 percentage points since February 2020. However, this is largely due to population aging, not the pandemic. Overall labor market participation rates are now in line with many prepandemic forecasts. As can be seen in Figure 2, overall participation is now slightly above CBO’s January 2020 projections for 2023Q1.[1]

As we discuss in the recent Economic Report of the President, demographic headwinds from population aging continue to pose a labor supply challenge for the U.S. labor market in coming years. The baby boom generation is aging out of the labor force, and the cohort of younger workers coming up to replace them is much smaller. This could pose a real challenge for industries with older workforces. Policies targeting barriers to labor supply, such as public investment in accessible, affordable childcare, and increasing immigration pathways are therefore warranted.

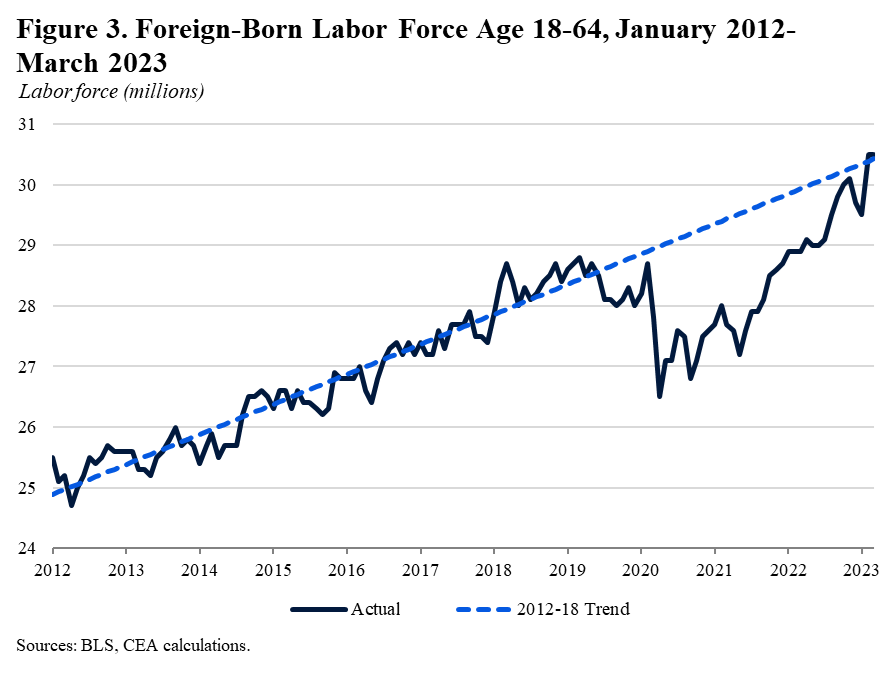

Immigration bans and restrictive policies of the prior Administration decreased the flow of foreign-born workers who were critical for many industries, particularly food services and agriculture. Due in part to the Biden Administration’s efforts to reduce unnecessary barriers and accelerate visa processing, immigration flows have rebounded from the pandemic. As can be seen in Figure 3, the foreign-born labor force has now largely returned to 2012-2018 trends. This rebound in immigration flows has helped to ease labor supply pressures.

The strong economic recovery has been good for workers in more ways than job creation. The gap between Black and white unemployment has narrowed considerably, and the unemployment rate for Black workers reached a series low of 5 percent in March (the series begins in 1972). The largest wage gains over 2022 went to Black workers, young people, and low-wage earners, reducing earnings inequality. There has also been a remarkable recovery in female labor force participation; last month the employment rate for prime-age women was the highest it has been since April 2000.

In other words, by many metrics, including those that formerly highlighted concerns about “missing workers,” the current labor market is the best for working Americans in many decades.

[1] CBO’s January 2020 projections reflect both expected demographic changes as well as CBO’s judgements about non-demographic factors affecting labor force participation. Moreover, subsequent updates by the Census Bureau to the Current Population Survey—in particular, the January 2022 population controls—suggest that overall labor force participation in recent years was in fact higher than previously thought. Were CBO’s January 2020 projections updated to incorporate these revisions, they would show a higher participation rate than the original published estimates.